Blog

Car Care Plan’s Conduct Risk Officer, summarises the FCA’s expectations in respect of the GI Distribution Chain

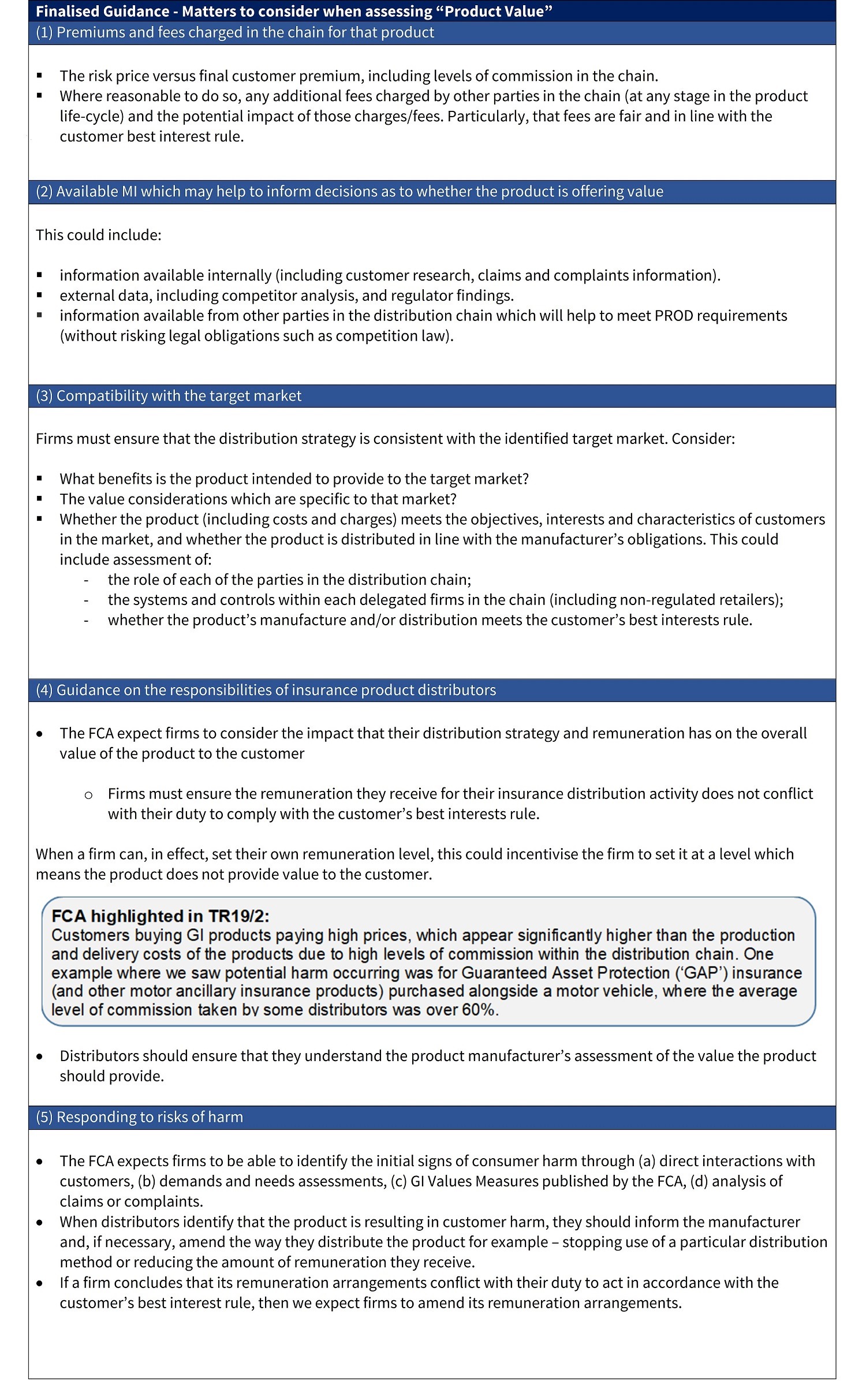

Following several years of focus, the Financial Conduct Authority (FCA) has published their “Final Guidance” in respect of the General Insurance (GI) Distribution Chain. Regulatory focus on this area accelerated after the implementation of the Insurance Distribution Directive (IDD) in 2018, which introduced the “customer best interest” rule, among other areas.

The FCA’s 2019 Business Plan looked at the impact of distribution costs on product value, leading to their Thematic Review (TR19/2 General Insurance distribution chain) in April along with a ‘Dear CEO letter’ and now their Finalised Guidance (FG19/5 The GI distribution chain).

FCA Timeline

The FCA’s Message:

In April, the FCA alluded to the “possible harms” highlighted in the above publications and;

- stated that many GI firms had not responded appropriately to consultation papers, resulting in regulatory action being taken in some cases;

- reiterated that the IDD had introduced new rules and responsibilities in relation to manufacture and distribution of GI products, including the “customer best interest” rule;

- reminded firms that the Senior Managers and Certification Regime (SM&CR) increases the obligations and individual accountabilities for senior managers.

The FCA also set out the expectation that all GI firms:

- must act fairly, honestly, and professionally in accordance with the best interests of customers;

- should consider the value customers receive from their products and services;

- should maintain appropriate systems and controls over the remuneration they receive;

- must maintain appropriate systems and controls (including the production and use of appropriate management information) over their GI products and services, including when delegating authority to another business;

- should consider the impact of their distribution strategy (including the distribution method and the level of remuneration they receive) on the overall value of the product for their customers;

- fully review the CEO Letter, the report, and attached guidance and identify and address any gaps.

Introducing the Finalised Guidance:

The finalised guidance was published in November 2019 (FG 19/5). It seeks to address potential customer harm arising in distribution chains from (a) failure in product design, (b) a lack of robust oversight of the distribution chain, (c) poorly designed product distribution strategies, and (d) conflicts of interest caused by remuneration structures.

It is designed to complement, rather than override, the requirements of IDD and the FCA’s RPPD – both of which remain in force. IDD rules already require that the distribution strategy of the product should be consistent with the identified target market (PROD 4.2.15R) and the product’s manufacture and/or distribution is compliant with the customer best interest rule.

The FCA have also stated that, while this guidance is specific to distribution chains, they expect firms to consider “product value” to the end customer for all sales types, both direct and intermediated.

Product Value – FCA Definition: By ‘value’ we mean the interaction between the overall costs to the end customer and the quality of the product and services. This stems from the effects of the rules which apply to manufacturers and distributors and the overall consideration of what is being provided to customers.

Saqib Basharat – Conduct Risk Officer

To stay up-to-date with the latest industry news and views, sign up to our newsletter.